Bajaj Auto stock is showing great momentum. Bajaj Auto has posted 86% growth in domestic sales for the month of June 2018 compared to corresponding month last year.

The company has risen the price of its flagship model, the Dominar, by ₹ 2,000 since 1 July, 2018. In 2018, the company has increased the prices third time by the same amount. This reflects great demand of the model. Currently, the Bajaj Dominar in its standard variant is available at the price of ₹ 1.48 lakh and the ABS variant is available at the price of ₹ 1.62 lakh. The competitors of Bajaj Dominar are Mahindra Mojo and the Royal Enfield Thunderbird 350.

Moreover, the entry level brands like Discover with 110 cc engine and Discover 125 were relaunched in 2018. The company had planned to expand their market share by 400-500 bps after the launch of new Discover bikes.

Strong Sales Numbers in the month of June 2018

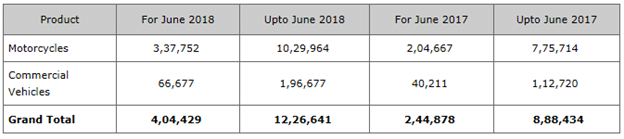

The company sold 200,949 units domestically during June 2018 as compared to 108,109 units sold in June 2017. The company also witnessed strong rise in exports on YoY basis. There is 42% rise in exports in June 2018 to 136,803 units. Overall, the company has delivered 65% growth in the domestic sales and exports combined together to total of 337,752 units in June 2018. Further, Bajaj Auto has registered highest ever quarterly sales for two-wheelers for the quarter April-June 2018. During this quarter, the company sold 10,29,964 units of motorcycles, with a growth of 33 per cent over the sales of April-June 2017.

Additionally, Bajaj Auto in the Commercial Vehicle segment has delivered 74% growth in the quarter April-June 2018 to 196,667 units including domestic and exports. The company for the month of June 2018 has posted 66% growth in sale of CVs including domestic and exports. Domestically, in the CV segments, the company has witnessed 78% rise in unit sold and 55% growth in exports.

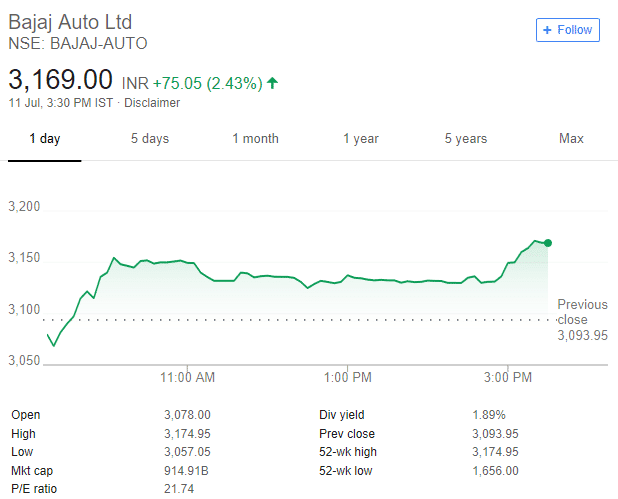

Bajaj Auto Stock Price Chart

Source Google Finance

The company’s demand in FY 19 is positive due to strong rural demand, expectation of normal monsoon for the third year in a row, and a healthy pick-up in economic activities. However, the key risks are inflationary fuel prices and higher interest rates. Seeing the demand and sales momentum, the company is expected to perform well in the near future.

The investors should accumulate the stock and buy on dips with a target of INR 3500

Disclaimer: The content on Financeminutes.com is provided for informational purposes only and it is not intended to be, and does not, constitute financial advice or any other advice