The Budget for 2017-2018 was presented on February 1, breaking historical practice. There is possibility of further advancement of budget in 2018. The Budget is normally presented for Financial year of the government which is defined as period starting 1st April and ending 31st March of the following calendar year

As part of the Financial Management re-engineering efforts by the government, there is impetus for challenging status quo and revisit ‘What should be period categorized as Financial Year for the government?’. It is not the first time this is getting challenged.

Background

When & who decided this to be financial year for India?

The present financial year in India (1st April to 31st March) was adopted by the Government of India in 1867 principally to align the Indian financial year with that of the British government. Prior to 1867, the financial year in India used to commence on 1st May of the current year to 30th April of the following calendar year.

This definition of Financial year has been challenged many times since but has stood the test of time for valid reasons or not. Pre-Independence it was challenged in 1870, 1900, 1908, 1913 & then in 1921.

Post-Independence this got lot more attention. It was challenged many times – in 1954, 1956, 1958, 1966, 1977, 1979, 1984 and a committee was set up on most occasions to do a detailed study.

Experts believe that the most comprehensive study was done in 1984 when a committee was set up under the chair of Mr. L.K. Jha

Most recently in 2016, a committee was set up under Mr. Shankar Acharya to do a detailed study on this topic. Report has been presented to Ministry for perusal in December 2016 and yet to be made public.

In the meantime, NITI AAYOG has come up with a discussion note on this topic in 2016 so as to socialise & sensitize various stakeholders on the merit of this topic.

Recommendations of various committees

It is interesting to note that almost all committees set up in the past (2016 committee report is not public yet) recommended a change in definition of financial year. Considering various factors, conclusion / recommendation is that April-March is not suitable. Surprisingly, despite so much attention, followed up with recommendation to change, the financial year has not changed

The recommendations have not been unanimous. The most recommended option is to sync Financial year with Calendar year (i.e.) January – December. Other suggestions such as Oct-Sep, Nov-Ovt, July-June have also been put on table.

Recommendations to change Financial year has not been implemented primarily under the pretext of a) ‘Why fix when it isn’t broken’? & b) Cost-benefit analysis not favouring the change in financial year

Thought process – What determines the ideal Financial year?

There are a few factors that are considered in analyzing and determining an ideal 12 month period for Financial year:

- The key determinant factor is the Nation’s BUDGET process & impact of Financial year on Budget process

- The importance of Agriculture and its seasonal elements in Budget process

- Impact of Financial year on Statistics & data collection periods

- The impact of Financial year on Business

- Tradition / Cultural practices

- International Trends

Analysing each factor in detail:

1. Budget

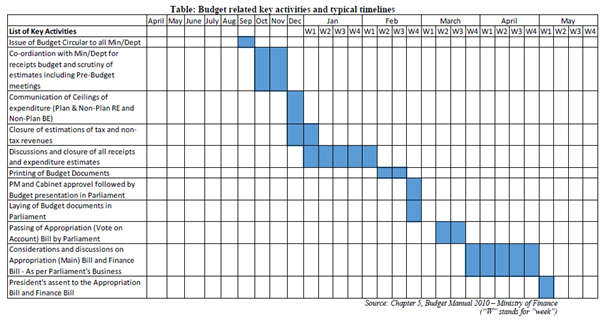

The union budget is very important as part of overall Governance where estimated receipts & expenditure of the Government for a financial year is presented to the Parliament. The Union Budget is one of the most important policy tools of the Government and is intended to support optimal allocation of scarce resources considering the social, economic and political priorities. The process is not short and takes about 4-5 months before it is presented. Typical budget time table is

2. Importance of Agriculture & its seasonal elements

There is a lot of negative criticism for importance given to Agriculture as a determinant factor of Financial year. Primary reason for the criticism is that Agriculture is not a material component of GDP at around 16-18%.

I personally feel that Agriculture should be seen beyond economic perspectives & GDP numbers. India is still Agriculture based economy with almost 45-50% of Nation’s employment dependent on Agriculture. It continues to dominate the socio-economic dynamics. In short, Agriculture is an important factor in any policy matter impacting the people in general

In India Agriculture is monsoon dependent and has 2 major cultivation seasons coinciding with the monsoon seasons – a) ‘Kharif’ season covering July – Oct coinciding with South west monsoon that accounts for about 75% of total rainfall of the country, b) ‘Rabi’ season covering Oct-Mar coinciding with North east monsoon & dependent on how good the South west monsoon was.

The proportion of agricultural total output is almost equal in both ‘Kharif’ & ‘Rabi’ cultivation seasons. However different crops have different trends.

The idea is that since the dependence on monsoon is so heavy, if there is a bad monsoon year the Government’s support mechanism should be able to get timely data, act timely & the welfare measures reach the impacted farmers & consumers on a timely basis.

The argument in all committees reviewing the ideal Financial year is that April-March is worst placed for this purpose. If there is a bad monsoon in a year (Jul-Aug-Sep), the welfare measures will take almost 8 months (May-June) as the welfare measures through the Budget has to wait till it goes through the cycle.

Unfortunately, there is no consensus (understandably) on what is an ideal financial year to address agricultural need. This is owing to monsoon dependent cultivation seasons. There are arguments for a July-June, Nov-Oct & Jan-Dec financial years on this topic alone.

I feel that there is misplaced emphasis of reaction & response to bad monsoon. Bad monsoon should be viewed as exception and there are exception handling mechanism in place like disaster relief measures. If they are falling short they should be improved separately and that should go into the budget planning. Budgeting process should be strategic enough to address the root causes systemically and not be transactional to provide ‘Band-aid’ fix.

3. Statistics & Data collection periods

The National Accounts Statistics (NAS) refers to a gamut of data collected and disseminated with different periodicities (yearly, quarterly, monthly etc.) and for different levels of the federal system of the country (centre, states etc.). Such statistics include data accounts of macroeconomic indicators such as GDP, GVA, consumption, GNP, per-capital income, agriculture crop production and so on. These statistics are compiled by the Central Statistical Organization (CSO) with reference to the recommendations and guidelines of the United Nations System of National Accounts (UN-SNA).

The CSO acknowledges the difficulties in synchronizing statistics of all sectors with the existing financial year. However, the CSO does not think that this particular issue poses any serious limitations to the quality/efficacy of the data for the purposes of statistical reporting in the national accounts. The UN Statistical Office and the various UN Organizations were in favour of presentation of statistics on calendar year basis as they followed the calendar year for presentation of international statistics in all their statistical publications.

Hence this becomes an indifferent factor with only a preference for Jan-Dec financial year.

4. Impact on Business

Business community has been quite vocal in raising their concerns on this topic and their preference is to maintain Status-Quo (i.e.) April – March. There are valid arguments;

- Companies Act 2013 mandates companies to follow financial year of the government as the financial year of the company (with some exceptions). This is a deviation from earlier stance which provided flexibility to companies to choose their respective financial year. Flexibility for companies to choose their financial year is common internationally as well. In this context, change of Government’s financial year forces companies to change their financial year and that has serious cost & business disruption implications, especially when a lot of resources have just been spent in the last few years to comply with Companies act 2013

- There are already enough major changes going through in the industry with Demonitisation, GST, Ind-AS etc. Hands are full and changing the financial year is viewed as a ‘Huge Avoidable disruption’. It has material transition cost implications as accounting, book-keeping, taxation, HR processes & systems have to be changed

ASSOCHAM has openly opposed the proposal to change Financial year and has compared it to changing driving system from right side to left side.

Business should be given flexibility to choose their financial year that suits their industry and one that facilitates right presentation of financial information to its stakeholders.

From a Regulatory compliance perspective, they must follow Government’s financial calendar and related expectations which goes without saying. Even top companies in Fortune 500 neither have same financial year nor have one that matches with their Government’s financial year.

5. Traditions / Cultural practices

I personally feel this is the best judge as law of the land should be quite close to culture of the land. However, India is as diverse as any country can get and there is simply no one single unanimous tradition / cultural practice that indicates what could be Government’s Financial year.

There is a practice in the business community to treat Diwali as a new year especially for accounting. Hence, there is an option of choosing a consistent date in the Gregorian calendar around Diwali time – say 1 Nov and have the financial year as Nov-Oct. This has been a recommendation in few of the committees. However, I differ from this view as there is no significant advantage – financial or social or psychological, of moving the Government’s financial calendar. Further this thought process still does not represent India well enough as it is more diverse.

Considering harvest festival timing to choose a Financial year will also not yield a simple choice as it is quite diverse. There are harvest festivals in Aug, Dec, Jan. The existing financial year is closer to Indian New year celebrated in different parts from Feb-April.

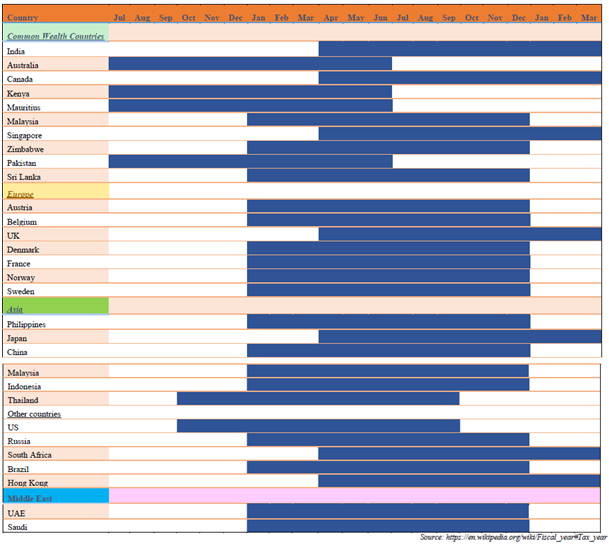

6. International Practices

There is no global standard as such for financial year. Different countries choose different period as Financial year. There is no regional consistency as well. Jan-Dec seems to be most favourite option & April – March is the second most favoured option

Source Wikipedia

My view on way forward

I think this topic of changing Financial year has been taken up way too many times in the past. The recommendation on most occasion was to change it but it was not changed.

I don’t think there is enough merit or pain currently that warrants more effort to revisit the financial year definition & more so to change it. I don’t think the ‘Problem statement’ is material enough or clear.

There is no perfect solution to this and we must choose a period and move on. I think we have a financial year and we can very well stick with it. If addressing the farmer or people welfare in a bad monsoon year is a key problem area, changing financial year is not a strong enough solution. The nuts & bolts of our welfare machinery has to be checked and corrected.

On a related but tangential note, budgeting process suffers from a key limitation that needs addressing on priority. Changing the ‘Accounting Methodology adopted by government’ would plug a lot of gaps which the machinery is facing today.

What is wrong with the Accounting methodology of the Government?

I intend to write on this topic in detail in future. Touching on it briefly Government follows ‘Cash based accounting’ and not ‘Accrual based accounting’. Anyone getting exposed to Accountancy even for the first time knows that ‘Accrual accounting’ is the more prudent form of accounting. However traditionally Government accounting of many countries has been cash based for many historical reasons

Cash accounting recognizes a transaction only when money changes hands, accrual accounting recognizes the transaction at the time it is made, thereby providing a more current snapshot.

Almost all the Finance Commission reports (latest being 14th) recommends and talks about this. There was some action on this topic in 2007-2012 but it seems to have gone quiet in the recent past. The change of accounting is by no means straightforward. Estimate is that it will take 10-15 years to achieve accrual based accounting in both state & central level but we have to start and start soon.

Advanced countries have moved to or in the process of moving to Accrual based accounting.

In India, we have done pilot study in 2009-2010 in State of Andhra Pradesh and Forest & health departments of Madhya Pradesh. For an accountant & auditor in me, the gaps from the pilot study are alarming which are just tip of the iceberg. But this this a (with associated pain) that the Financial Management of the country must undergo.